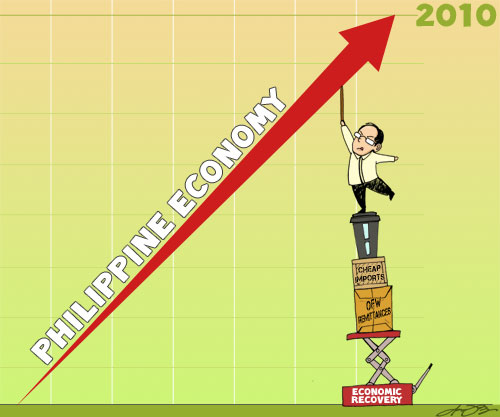

Two incendiary changes this year helped jump-start the Philippine economy — down but not out — as it reeled from the global financial meltdown that began in the US in 2007. The most obvious was the changing of the guard in Malacañang, with then President and now Pampanga 2nd District Rep. Gloria Macapagal-Arroyo completing her nine-year rule. President-elect Benigno Aquino III and his Cabinet came in as a breath of fresh air and a band of purported idealists. But idealism alone cannot rescue hostages. In the aftermath of the Aug. 23 hostage-taking incident, Sen. Joker Arroyo branded them the student council in Malacañang.

Analyn Perez, GMANews.TV

While he wasn’t purely a political novice to the core, Aquino’s record as a representative and a senator was clearly unblemished for having achieved hardly anything during his cameral term. In

his inaugural speech on June 30, 2010, Aquino vowed to stamp out corruption, follow the straight and narrow path, and spur the economy that nearly gave in to the shocks of the financial crisis that spurred a global recession to which the world’s largest and strongest market economies in Asia, America, and Europe had succumbed. He promised to curtail government spending, with the national coffers nearly broke and

a gapping deficit of P325 billion equivalent to 3.9 percent of the economy in GDP or gross domestic product terms. There was a kind of euphoria in response to the pronouncements of the 50-year-old bachelor from Tarlac and Quezon City. At least, he wasn’t merely ranting but staying true to his word when it came to his vows to eschew the

wangwang and counterflow that for many Filipinos came to symbolize the arrogance of power under the Arroyo and previous administrations.

Impact of the May 10 polls For many of the 90 million or so Filipinos, he was becoming a symbol of hope, a harbinger of change. The impact of the May 10 elections that brought PNoy to Malacañang was reflected by the stock market the very next day. The Philippine Stock Exchange index or

PSEi surged 120.87 points to 3,262.95, a 3.85-percent gain that was the biggest for the measure in nearly nine months. “First, finally elections are over," Astro del Castillo, managing director of stock brokerage First Grade Holdings Inc., told GMANews.TV at that time. “That’s one less headache for us. And it has been peaceful and orderly." There was a clear mandate for PNoy, lending a semblance of political stability, popular support, and business confidence. The timing augured well for the Philippines, whose

agriculture sector had just been devastated by a prolonged drought from the El Niño phenomenon and a series of typhoons, mostly in the main island of Luzon. Plus, the

export sector was nearly annihilated as overseas customers whose economies were down on their knees lost the capacity to place their usual orders. Many Philippine companies instituted drastic cuts in working hours to curtail operating expenses, a lesser evil compared to a total retrenchment.

The missing ingredient The other shift was in the direction of foreign investments. As the US economy continues to falter on its way to recovery and the euro debt crisis continues to raze Europe’s market economies, those magic words — political stability, popular support, business confidence — convey a kind of magic to foreign and domestic fund managers. The missing ingredient in the form of solid macroeconomic numbers, however, was not yet there. It arrived 17 days after the May 10 elections, and just over a month before Aquino was to deliver his inaugural address in taking the helm of government. Its harbinger was the National Statistical Coordination Board or NSCB, reporting on May 27 that the

Philippine economy in GDP terms grew 7.3 percent during the first three months of the year.

A quarterly comparison of the Philippines' GDP. Source: NSCB. Graphics: Einstein Rojas, GMANews.TV

Considering the

economy was almost stunted at 0.5-percent growth in the same quarter a year earlier, and with most of the world economies still suffering from the impact of the depression, it was hailed as a surprising rebound for the Southeast Asian nation’s economy. The National Economic Development Authority (NEDA), a Cabinet department, earlier projected the economy was likely to grow between 2.9 percent and 3.9 percent in the first quarter of 2010. It was not a result of Aquino winning the presidency but a confluence of the global economy slowly recovering from the depression, business and consumer confidence encouraged by the impending change, and the most obvious: election-related spending. The flow of goods and services has stirred growth this way, as explained by NSCB director-general Augusto B. Santos: "The economic growth in the first quarter of 2010 translated to an increase in employment of almost two million (1,730,000). Employment creation was seen more on services, followed by industry." He also did not miss the point that the Philippine economy is primarily consumer-led, the kind that depends a lot on the money sent by overseas Filipino workers to their families back home — obviously, as local salaries based on the mandated P485-a-day, minus taxes and other deductions, simply pack little spending power. “The continued strong inflows of remittances and the increase in employment particularly in services both fueled consumption," Santos said in reporting on the first quarter GDP. The first quarter GDP results were not about the impact of Aquino but the macroeconomic fundamentals that fund managers had been waiting for to cue them in. Money from abroad deluged the stock market, pushing the PSEi to break its own record highs. The chief market strategist of BDO Universal Bank, Jonathan Ravelas, told GMANews.TV on June 3 the market was still riding on the positive impetus of the 7.3-percent growth in the gross domestic product for the first quarter, with investors expecting the economic conditions to have a compelling impact on corporate earnings. He was speaking on the day the PSEi rose 65.67 points, or 1.99 percent, to close at 3,355.23.

World Bank warns vs risks With foreign funds obviously stirring up equities markets not only in the Philippines but also in East Asia as a whole, where economic prospects hold more promise than in the US and Europe, World Bank economists raised their forecast to 8.9 percent from 8.7 percent for the region. "The economic recovery in East Asia and the Pacific is robust, but attention must now turn to managing emerging risks which may pose challenges to macroeconomic stability,"

the multilateral lender said in its outlook for East Asian economies, excluding Japan. Asia's rebound has attracted an influx of capital that is pushing up the value of some currencies, which might hurt exports. Some governments have intervened in foreign exchange markets to slow the rise of their currencies, raising fears of a potential "currency war" that might disrupt trade and growth, the Associated Press reported on Oct. 19, citing the WB outlook. In such a situation, the bank called on East Asian countries to control such risks with a common approach so as not to derail the export sector’s recovery. [See

Exports, OFW money to boost peso, foreign banks say] The flow of money into East Asia also threatens the regions’ banks as borrowers might in the end bear the cost of servicing such huge sums of capital, increasing the likelihood of non-payment of loans, according to the bank.

Manix Abrera, GMANews.TV

Despite the concerns raised by WB on currencies, LaidTrades.com analyst Ron Acoba saw things in a different light, the peso in particular. “One main factor that is affecting the peso exchange rate is the level of remittance (dollars) from abroad that is sent back to the country. For those who do not know, about 11 percent of the country’s gross domestic product or simply total output comes from the money sent home by overseas Filipino workers (OFWs)," according to Acoba’s analysis on the global equities and foreign exchange forum online. In a separate commentary, Alcoba said the Philippines “is not an export-based country so even if the country’s export sector gets negatively affected, it would not reflect badly on its overall output." A stronger peso would make imports cheaper and encourage more consumption, at the same time allowing Philippine “companies to better access and purchase technology that were once scarce, making the processes of local industries more efficient," the LaidTrades analyst explained.

OFWs sent home $15.456 billion in the first 10 months of the year, up 7.9 percent from $14.231 billion a year earlier, according to the Bangko Sentral. The money sent home by OFWs totaled $1.673 billion in October, a new monthly record signaling the advent of money transfers for the Christmas season, the central bank said in a report on remittances. “Christmas is very much celebrated in the Philippines since more than 90 percent of its population are Catholic. Christmas shopping and giving gifts to family and friends have always been an indelible part of Filipinos’ culture," said Acoba. With that kind of tradition at play, “remittances from abroad will surely soar during the holiday season… More money spent would then benefit the individual businesses and the whole economy in general which would likewise reflect on the currency (peso)," according to Acoba. “Moreover, improved consumer sentiment during this season would lead investors towards the higher yielding assets and away from the US dollar. Such would also indirectly benefit the peso exchange rate," he added.

— HS, GMANews.TV